Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

Last week was a blockbuster week for NTUI! President Jim Tobin spoke at the Rockford Tea Party on April 6, we were featured on WLS TV (ABC 7) April 7, and the following column ran in the Wall Street Journal on April 8.

In Praise of Illinois

Democrats take baby steps on pension reform.

The Pew Center on the States recently honored Illinois as the state with the biggest public pension mess. So it’s a minor miracle that the state’s Democratic legislature passed, and Democratic Governor Pat Quinn is expected to sign, a pension reform that at least takes baby steps in trimming the state’s retirement largesse for its 700,000 government workers. Perhaps bankruptcy concentrates the mind.

A new report by Charles Wheeler of the University of Illinois Springfield summarizes the state’s problem this way: “To say Illinois faces a hole in funding its public employee pension systems is like saying the Grand Canyon is an impressive ravine.” He finds that the state’s five retirement systems “will need roughly $131 billion to cover benefits already earned by public workers, with only $46 billion in expected revenues to cover the costs.”

In other words, the state only has about 35 cents for every dollar it must pay in the future. If Illinois were to devote every penny for three years from its income and sales taxes, it still wouldn’t have enough to met these unfunded liabilities. No wonder the state’s credit rating is the second worst in the nation, behind only California.

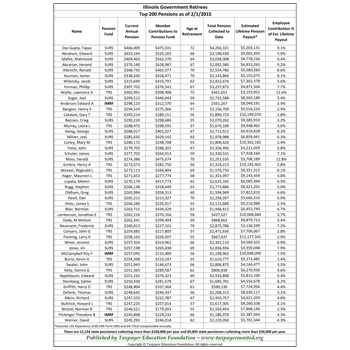

State workers can retire with full benefits at age 55. Most get an automatic 3% wage increase each year, regardless of inflation. Workers can and do get retirement benefits while still working full-time for the state. More than 3,500 state workers pocket annual pensions of more than $100,000, and the highest pension is $391,000 a year, according to National Taxpayers United of Illinois.

It took public outrage over these benefits and a chronic budget deficit of $6 billion to get the legislature to act. The reforms include increasing the retirement age for full benefits to 67; capping annual pensions for the highest paid workers at a still high $106,800, and prohibiting double dipping on a pension and public paycheck at the same time.

Illinois unions are furious and are blasting what they call a “pension slashing bill” that benefits the “elite corporate class,” as if middle-class taxpayers are elites. The union solution: Raise taxes. Democrats rarely oppose union demands, so even though these pension reforms are far short of what’s needed, we’ll salute them. Let’s hope this is the start of a nationwide backlash against the scandal of runaway public pensions.