Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

Click here to view release as a PDF

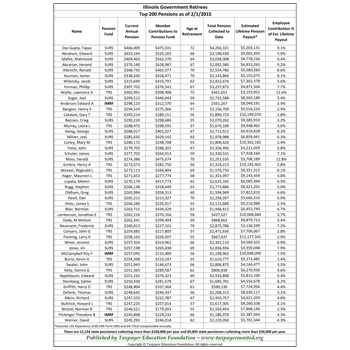

Frankfort–A report released today by Taxpayers United of America (TUA) reveals that Frankfort, Franklin County and Kentucky State government employees are not only receiving generous salaries, but that over a normal lifetime, many of these government employees when they retire will become pension millionaires. Kentucky bureaucrats refuse to release pension figures, so total pension payouts were estimated* for this report.

Click below to view the pension information:

“While Franklin County taxpayers struggle through this recession with an average wage of $39,000, a median home value of $133,000 and 7.6% unemployment, government employees really rake it in while they are employed and then when retired,” said Christina Tobin, TUA Vice President.

“Starting first with the top 100 salaries and estimated pensions (2010) for the university employees, heading the list is Michael Karpf, whose salary is $776,913. When he retires, he will receive an estimated annual pension of $446,148. Karpf’s estimated total pension payout over a normal lifetime is $12,585,995.”*

“Frankfort City Manager, Anthony R. Massey earns an annual salary of $ 117,728. Massey’s estimated annual pension is $77,700 and over a normal lifetime will total an estimated $3,108,010.”**

“Franklin County Clerk, Guy Zeigler, is on track to receive an estimated $2,630,409 lifetime pension payout for his annual salary of $99,637.”**

“Jefferson County teacher, Janice James tops our list of Kentucky government school teachers at an annual gross wage of $ $95,179 and estimated lifetime pension payout of $2,855,358.”**

“Franklin County government teacher, Elana Brock will rake in an estimated lifetime payout of $2,244,788 on her annual gross wage of $74,826.”**

“Kentucky government pension systems are making millionaires out of public employees at taxpayer expense. Although some reforms have been made to the Kentucky government employee pension systems, additional reform is critical. Ending pensions for all new government hires would eventually eliminate unfunded government pensions; putting new government hires into social security and 401(k)s would achieve this. If each current government employee were required to increase contributions toward his or her pension, taxpayers would save billions of dollars.”

“We need to knock all politicians out of office who make deals with bad government union bosses and bad corporate power brokers at the expense of the taxpayers.”

*Assumes retirement at age 62 after 30 years, Life expectancy (IRS Form 590) 23 years

**Assumes retirement at age 52 after 30 years, Life expectancy (IRS Form 590) 32 years

These numbers are really bothersome because of their vast inaccuracy. Being someone who has calculated Kentucky state employee retirement for many of my friends (very accurately, I might add), I can tell you both your assumptions and your numbers are far off.

Let’s hit the assumptions, first of all:

1. “Assumes retirement after 30 years.” Most people retire at 27. Retiring at 30 means more income than at 27, a fact of which I’m sure you’re fully aware.

2. “Assumes retirement at age 52, life expectancy 32 years” First, that would mean all employees start state employment at age 22, which is clearly incorrect, especially for the higher paying positions they studied, such as attorneys, doctors, and appointees. You can’t graduate medical school at 22, nor law school, nor do I know a single political appointee that is 22 years old. Second, are you saying the average life expectancy is 84 (52 + 32)?? Kentucky is lower than most other states due to smoking and obesity, and certainly not near 84 years old. I just checked the number, and it continues to go up, but in 1996 (most state employees are older than that), it was still only 67 for men and 74 for women. Nowhere near 84.

3. “Assumes COLA of 2% per year (1.5% guaranteed plus .5 add-on)” we have rarely gotten 2% in any of the 10 years I’ve worked for Kentucky, and 1.5% is FAR from guaranteed. We got 0% these last two years on top of roughly a 6.5% pay cut. Another bad assumption simply meant to increase your numbers.

4. “Assumes last salary is avg. salary” Again, not usually the case, although if we keep getting 0% raises, then it could turn out to be accurate. The state averages your top 5 years (called the “high 5”), and again, this is far lower than your assumption that one’s retirement is basely solely on your highest year.

All 4 of these assumptions raise their estimated salaries far beyond reality. To be more accurate, for older employees, your pension is *roughly* about 52% of the average of your top 5 years (it’s less for new employees). Also, looking at your list of “estimated top 25 pensions”, did you notice that it looks like all or almost all of those employees are CITY employees, not state employees? The city has a somewhat different retirement plan.

It’s very disappointing to see your organization attack state employee pensions, when the job already pays far below average wages. The pension plan is about the last decent method of recruitment that the Commonwealth of Kentucky offers, and it’s constantly under fire from organizations like yourself. The average retirement income of state employees in Kentucky is $20,400. That’s not a ridiculously large amount of money on which to retire, folks.

Brian,

Estimated pensions were calculated using all known data and current KY law as well as IRS 590 for life expectancy. Of course, there will be differences in some of the pensions because one has to rely on facts known and assumptions consistent with the laws, rather than individual circumstances and opinions. So the estimates are accurate based on the proper calculation of the known data points.

The solution though, is for Kentucky government to release the actual pensions, then estimates would be moot. In either case though, it is a matter of simple mathematics that defined benefit pension systems are causing governments to go broke. Maintaining and defending this type of pension system only considers those who collect from the system. Changing to a defined contribution system protects the taxpayers and the government employees.

Further, the response from the governor’s office “…did not dispute the group’s estimate of his pension.”

In the private sector, if you graduate from college at 22 then you work 40 years to early SS retirement, Max. Social Security pension is 22,000. That is the max that anyone can earn, regardless of past wages and contributions.

The matter of wages is a different discussion and should be evaluated separate from retirement benefits.

Rae,

Thank you for the response, but you are making bad assumptions. Retirement pay is based on wages, so they are not different issues at all. The fact is that Kentucky state employees have received little to no wage increments for the last decade, and that has been devastating to our future retirement income. Mine, for example, has been halved. As someone in a technical field with two degrees, I expected to have a comfortable retirement. At this point, I will not be able to stop working at retirement age (57 for me) due to all the increment and pay cuts (that, as I said, will affect our retirement income dramatically).

Hopefully, you now understand the link between currently earned income and retirement income.

However, you did not address any of the bad assumptions you made. Do you really think it’s possible that doctors will start working at 22 years of age? Or attorneys? Again, these are bad assumptions that seem to have been made simply to inflate your numbers. I understand if you have to make assumptions, but you shouldn’t assume people will work 30 years in a system that allows them to retire at 27, and that people with 10 years of education will somehow start state employment at 22 years old. Doctors have 4 years of college, then 4 years of medical school, then 2 years of residency. That means a typical doctor could start work at 28 years old, at the earliest. Why did you assume they would start work at 22? And that lawyers would, and political appointees would? They don’t.

I also fail to see your point about social security earnings. We’re not talking about social security–we’re talking about a pension plan that was promised to employees of an organization upon being hired.

I have no idea why the governor doesn’t release the actual pensions. It would clearly show, at least for the rank and file employees, just how wrong your numbers are. I don’t care if you have an axe to grind against the big shots in government, as long as you don’t attack average people like me who are trying to make a living. I sure wish I had some of those “Cadillac benefits” that people are always saying on message boards that state employees have, but the truth is, I had better benefits before I came to state government (at the age of 30, not 22).