Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

TUA’s work on California’s pension crisis is mentioned in this post at CalWatchdog.com.

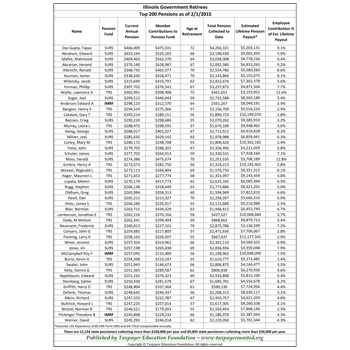

If you have not read or heard anything about California’s unfunded public employee pension crisis, you’ve probably been living under a rock or, like union bosses and too many members of the state Legislature, the governor’s office and local elected officials, you are happily in denial.

If you have not read or heard anything about California’s unfunded public employee pension crisis, you’ve probably been living under a rock or, like union bosses and too many members of the state Legislature, the governor’s office and local elected officials, you are happily in denial.

Tensions are mounting too as pension deniers or pension reform “obstructionists, as Mercury News writer Daniel Borenstein called them, are attempting to publicly shame those of us pointing out that pension liabilities could bankrupt California without serious reform.

Borenstein is joining CalWatchdog contributor Steven Greenhut and David Crane, a former California State Teachers Retirement System board member, and me for a panel on pension reform in San Francisco on Thursday.The unions have already gone on the attack about the event.

“Spotting my scheduled appearance on an upcoming conservative think-tank panel to discuss public-employee pensions, union spokesman Steve Maviglio went into Twitter attack mode last week,” Borenstein wrote for the Mercury News.

“@stevenmaviglio branded me a ‘pension basher’ and called my ethics into question. His sad attempt to divert the debate badly mischaracterizes my position and further undermines serious discussion of a complex issue.”

Fortunately as unions get louder so do the cries from taxpayers and advocacy organizations.

Christina Tobin, Founder and Chair of Free and Equal Elections Foundation and Vice-President of Taxpayers United of America, this week has been holding press conferences in California cities to draw increased attention to California’s pension crisis, including a planned event in Fresno on Wednesday and San Francisco on Thursday (in the morning before the reform panel).

Instead of denying the flood of economic problems looming because of pensions, it’s time to face the facts and fix the problem.

It was quite alarming to read the proposal of the Taxpayer United of America ”to move public employees from a defined benefit plan … to a defined contribution plan, known as a 401(k) plan.”

The Wisconsin Retirement System, aka the state pension plan – is a smashing success and a role model for all pension plans nationwide. It is the one invention that can promise a better life for hundreds of thousands of Wisconsin citizens.

In contrast, 401(k) plans are a Wall Street skim operation. The majority of 401(k) plans are distributed amongst millions of small businesses, which means there is no economy of scale. In addition, most individuals do not have the financial savvy to avoid the inherent investment risks. As a result, individual 401(k) plans buy stocks and bonds at retail prices and their 401(k) balances at retirement are woefully small. In contrast, Pension Plans pool large amounts of money – which enables them to buy stocks and bonds at wholesale prices and mitigate investment risk with highly skilled financial specialists.

Many pension plans were mismanaged which is why they became a burden on private and public employers. The solution is to modify those pension plans and copy the state of Wisconsin Retirement System (WRS). Bringing the WRS success to more Americans can be achieved through everyone’s representative trade organization. For example, for food workers, the National Restaurant Association has over 12 million members. The American Truckers Association has 37,000 members. That provides an economy of scale. The Newspaper Association of American could be a viable entity to organize a pension plan for you.

Tragically, for most Americans, a 401(k) plan will never give them the retirement security that is provided by the Wisconsin Retirement System.

I hope you can stop being gullible to pro Wall Street propaganda.

NOTE: There is no secrecy to the Wisconsin Retirement System. A simple way to calculate the approximate annuity of everyone who participates in the Wisconsin Retirement System (WRS):

“Average final salary” x number of years in the WRS x .0162 = approximate annuity at retirement.