Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

TUA’s study on Chicago police pensions was referenced in an article at The Globe and Mail.

It turns out Jane Jacobs was wrong. Rationalist urban planners weren’t the worst thing that ever happened to the Great American City. Pension-promising politicians have done far more harm.

It turns out Jane Jacobs was wrong. Rationalist urban planners weren’t the worst thing that ever happened to the Great American City. Pension-promising politicians have done far more harm.

That’s clear in newly bankrupt Detroit, which spends 40 cents of every tax dollar on retirement benefits and debt service costs. Is it any wonder the street lights don’t work?

Detroit is admittedly an extreme example, driven to its knees by decades of depopulation and political dysfunction. But its insolvency has drawn attention to the greatest threat to American cities since possibly the Spanish flu: unfunded pension and health liabilities for retired workers.

Short of declaring bankruptcy, it’s nearly impossible for cities to cut contractually protected pension and health benefits. So instead, they’ve been slashing basic services and/or cutting back on new investments in infrastructure, undermining the basis for future prosperity.

Even that hasn’t solved the problem, though. Estimates of the extent to which cities have failed to set aside enough money to pay pension and health benefits vary. But the gap easily amounts to hundreds of billions of dollars. Include state governments and the shortfall is into the trillions.

“Pension liabilities are widely acknowledged to be understated,” Moody’s credit rating agency said this month. It estimates the true shortfall at three times the sums reported by cities.

Last week, Moody’s downgraded Chicago’s credit rating by three full notches. The vibrant Windy City is no Detroit. But benefits for former employees and interest on its debt now suck up a third of its operating budget. And things will only get worse. Moody’s pegged Chicago’s unfunded liabilities at $36-billion (U.S.) – almost twice the $19-billion reported by the city.

Accounting gimmicks are one of the biggest reasons for the discrepancy. Cities have bet on a rate of return on pension investments above 7 per cent, although the yields on government bonds hover around 2 per cent. Not only have cities and states contributed billions less than they should have over the years to fund future pensions, but very few have set aside any money at all to cover retiree health benefits.

It’s no mystery how most U.S. cities and states got into this mess. For decades, politicians bought labour peace by promising higher pay and benefits for public employees without thinking twice about how to pay for them. Most knew it would become someone else’s problem anyway.

Whether public employees deserve their pensions is beside the point. (While the pensions of Detroit workers appear reasonable, they also reflect that city’s lower cost of living.) Still, politicians shirked their fiduciary responsibility for the financial integrity of their cities.

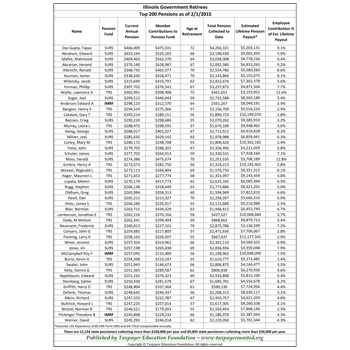

In Chicago, the average police pension is $55,000. For firefighters, it’s upward of $60,000. In 2011, 94 former Chicago police officers had pensions above $100,000, according to Taxpayers United of America. What’s more, unlike their peers in many other cities, retired Chicago police also receive partial federal Social Security benefits, up to about $13,000 a year.

Since police, firefighters and teachers typically retire in their 50s, many will draw pension and health benefits for three decades or more. That is, unless other cities follow Detroit, which is asking a bankruptcy judge to let it slash pensions. If Detroit gets its way, it will set a precedent other large cities may try to follow. Until now, all they’ve been able to do is squeeze concessions from unions that affect only new employees, who will retire later and contribute more to their pension fund. And in most cases, police and firefighters have been exempt from the changes.

The greatest reckoning may come in California. The state has already seen smaller cities such as Vallejo, Stockton and San Bernardino declare bankruptcy. Last year, almost 15,000 former California public employees drew pensions of more than $100,000. And the $100K club is adding thousands of new members a year as baby boomer retirements pick up steam.

Public pensioners can be expected to put up a fight wherever officials seek to cut their benefits. But it would be hard to top the sheer nerve of Bruce Malkenhorst, the former city manager of the Los Angeles-area industrial enclave of Vernon (population 112). His 2012 pension was $540,000, until the California Public Employees’ Retirement System cut it to $115,000.

Mr. Malkenhorst, 78, who has been convicted of misappropriating public funds, is now suing to recoup the difference, citing “elder abuse.” It does make one read Jane Jacobs and weep.