Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

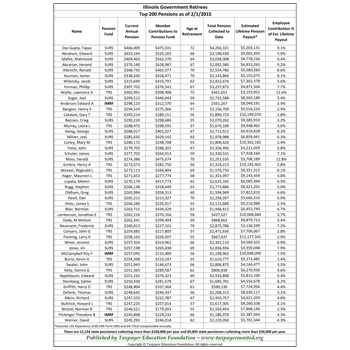

The coronavirus damage to Illinois’ already-critically-ill economy could push Illinois state pension debt to over $300 billion, according to a recent study published in Wirepoints. The study’s authors based their calculations on figures from Moody’s Investors Service.

“Never has the financial situation of Illinois been so dire,” said James L. Tobin, economist and president of Taxpayer Education Foundation. “The state’s condition demands significant tax cuts, not tax increases.”

“Yet, Ill. Gov. Jay Robert ‘J. B.’ Pritzker is pushing approval of his Income Theft Amendment to the state constitution, which is on the November 2020 ballot. This huge increase in the state income tax would wipe out Illinois’ middle class and make the State of Mississippi look wealthy by comparison.”

Moody’s most-recent calculation for the state’s pension debt before the crisis totaled $241 billion. The authors of the study calculate that the shortfall will jump to $312 billion in 2020, due to the stock market’s meltdown and collapsing interest rates.

“Pritzker plans to use the proposed income tax increase to pump more cash into the state’s bankrupt government pension plans, which provide lavish, gold-plated pensions to Illinois’ government employees, some of whom have retired in their middle 50s. This is totally unacceptable. State government pensions must be reduced to realistic levels, and all new hires need to be placed is 401(k)-type pension plans.”

“But none of this will matter if state and local taxes are not significantly reduced. Once the state’s middle class leaves, it will leave forever.”