Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

CHICAGO—Taxpayers United of America (TUA) today released the results of their updated study of the top pensioners of Illinois state pension funds, including SURS, TRS, IMRF, and GARS.

“Illinois leaders, Gov. Patrick Quinn (D), Michael Madigan (D), and John Cullerton (D), insist that we have a revenue problem,” stated Jim Tobin, president of TUA. “They point to the so called pension reforms passed last year, which have not curbed the growth of unfunded liabilities and in fact, Illinois’ government pension liabilities have grown to $187 billion.”

“It is unconscionable that these lawmakers, also known as The Most Notorious Tax Villains, support increasing the state income tax on as many as 85% of Illinois through a graduated income tax, or at the very least, making the ‘temporary income tax surcharge permanent.”

“It has never been clearer that the job-killing policies of raising taxes to prop up the gold-plated government pensions, and the union votes that follow, are more important to these Tax Villains than the future of Illinois itself.”

“How can any government bureaucrat look at the individual pension payouts and deny that this system is unsustainable? There are over 11,054 state pensioners now receiving more than $100,000 per year. By the year 2020, there will be 25,000. There are over 78,526 state pensioners receiving annual pension payments over $50,000. These lavish pensions are funded by taxpayers who get an average Social Security pension of about $15,000.”

“Illinois still has the second highest unemployment rates at 8.4%, the second highest property taxes in the country, and the lowest rating in the country for its general operating bonds. The tax and spend Tax Villains responsible for the financial fiasco need to be fired at the ballot box in November.”

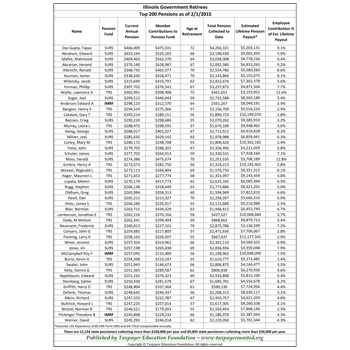

“What does $187 billion in unfunded pension liability look like to Illinois residents? Well, I’m sure you all remember Tapas das Gupta, who has topped our list since we have been publishing the list. His annual pension has grown to $452,843. Of course his estimated lifetime payout gets him a spot on millionaires’ row at, $5,276,384.”

View the State of Illinois Top 200 Government Pensions as of April 1, 2014.

“Not far behind Gupta is Edward Abraham whose annual pension is $439,965, or $9,073,587 in estimated lifetime payouts.”

“There are at least five government retirees in these funds that are on track to receive more than $10,000,000 in taxpayer funded payments. One such retiree may realize $11,535,660. Larry K. Fleming retired from Lincolnshire-Prairie View District 103 at the age of 55 and is now receiving $258,163 per year. He paid in a whopping $326,507 or 2.8% of his estimated lifetime payout.”

“These are shocking amounts for taxpayers to be on the hook. And while these represent the highest pensions, it does not diminish the fact that every Illinois resident, man, woman and child, share about $15,000 in unfunded liabilities for these state pension systems alone. On top of this is the unfunded liability for healthcare and the other 600+ local pension systems that don’t participate in the statewide pension funds. It is also shocking to realize that so many government retirees will be paid not to work for more years than they are actually employed!”

“Illinois’ government employee pensions are in dire trouble with no end in sight. Government employees, like the vast majority of taxpayers should save for their own retirement. Taxpayers simply can’t afford to pay so many, so much, to do absolutely nothing and retirees can’t afford the inaction of Illinois lawmakers who are afraid to alienate the special-interest money that keeps them in office.”

“Without sweeping and immediate reform, Illinois’ pension system will collapse. We need to fire Quinn, Madigan, Cullerton, and every one of the Tax Villains who support a graduated income tax or any other tax increase intended to prop up the failed government pension system rather than muster the political courage to end unfunded pension liabilities forever.”

“Pension reform must include raising retirement age to 67, increasing employee contributions by 10%, increasing healthcare contributions to 50% for employees and retirees, eliminating all COLA’s, and replacing the defined benefit system with a defined contribution system for all new hires. It’s mathematically impossible to tax your way out of this problem. Illinois has more than 11,000 retirees collecting more than $100,000 in annual pensions; in 2020, that will be over 25,000 six figure pensioners.”

*Lifetime estimated pension payout includes 3% compounded COLA and assumes life expectancy of 85 (IRS Form 590).