Jim Tobin, A Friend Of Liberty (1945-2021)

May 2nd, 2022

By: Christina Tobin

Sometimes a single man or woman has to stand up for principle, just so t[...]

States offer tax incentives with the goal of encouraging new investment and economic development in their state, but just because most states offer numerous incentives doesn’t mean doing so is the best approach, according to a report by the nonpartisan Washington-based Tax Foundation.

The foundation’s Katherine Loughead lists the major categories of incentives: Job creation tax credits; Investment tax credits; Research and development tax credits; Payroll withholding tax rebates; Property tax abatement.

The foundation’s research has shown that incentive-heavy tax structures undermine tax equity, with tax breaks for new firms driving up the tax burdens established firms pay.

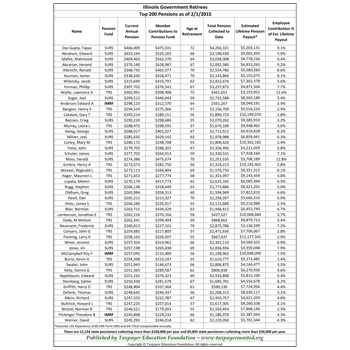

In most states, tax incentives abound, usually offered as a way of promoting new investment or attracting certain industries by shielding them from the full impact of otherwise high tax rates. Altogether, state and local governments give out an estimated $95 billion a year in business incentives. By way of comparison, state and local governments collected less than $66 billion in corporate income taxes in FY 2019.

Loughead states that “While proponents of incentives view them as a tool to promote desirable economic activities—like job creation and new capital investment—their effectiveness at achieving desired outcomes is dubious and difficult to measure. Numerous studies have shown that tax incentives often fail to live up to expectations for inducing job creation and growth… these incentives only reduce taxes for qualifying firms engaging in qualifying activities, meaning non-favored activities and businesses remain on the hook to bear the full impact of the state’s tax code.”

The foundation makes the following points:

The study concludes, “States that maintain a competitive underlying tax code will then find they can attract business investment and experience strong long-term economic growth without picking winners and losers and without cluttering their tax code with complex carveouts, a goal all states should work to achieve.”

“States that lower taxes for all will find businesses streaming in,” said Jim Tobin, economist and president of the Taxpayer Education Foundation. “There is no need for these targeted gimmicks.”

Source: https://taxfoundation.org/state-tax-incentives-costs/